| Financial Ratios | |

This

page last updated 2016 Oct 3rd

| Ratios - an introduction | Financial Ratios

are mathematical calculations of how a firm has measured some activities,

and compared those activities to other inputs, time periods, resources

etc.

In an increasingly complex

world were people are doing business on a global basis, with competition

from many direct and indirect competitors, it becomes more and more difficult

for investors and business partners to evaluate the "financial health"

of a company when they don't have the ability to meet the executives and

have probing discussions about what has been happening.

International finance in the 2nd decade of the new millenium, ie 2010+, involves fast decisions about companies all over the world for international investors, government fuind managers, stock traders etc.- ratios help these investors and fund managers make decisions in order to have the opportunity to avoid losing money in companies that may have trouble, and make money with companies that are profitbale now, and in the near future.In the absence of "going to the source" to find out how a company has been doing presently, and may do in the future, business executives have turned to a series of calculations, when taken together with other objective and subjective information, can give a better indication of a company's success or failure, than if you did not have this info. So the basic point is,

|

| Ratios

- an introduction

Limitations |

Ratios, without

context, are not enough information on which a business person can make

a confidendent decision. Ratios need to be provided in the context within

which the "numbers" are generated... a reference point is needed, as in

some sort of historical time period.

Secondly, the financial health"

of a company is more than just a series of mathematical calculations about

sales and expenses,

Again, the financial health" of a company is more than just a series of mathematical calculations as we can see in the example of companies that have had dynamic leadership which allowed the company to do well, even though there might have been times when the "books" were not attractive to institutional investors. examples

|

o Leverage Ratios (also called

Debt Ratios)(Leverage Ratios are also referred to as a type of "Solvency

Ratio"), including

o Capital Acquisition Ratio

o Capital Employment Ratio

o Capital Structure Ratio

o Long-term debt/capitalization Ratio

o Debt-to-equity Ratio

o Liquidity Ratios, including

o Current Ratio

o Quick Ratio (or "Acid Test"

o Cash Ratio

o Efficiency Ratios (also known

as Operating Financial Ratios),

(also sometimes titled

Asset Utilization Ratios or Asset Management Ratios)

o The Days Sales Outstanding Ratio

o Inventory Turnover Ratio (also referred to as Asset Turnover Ratios)

o Receivables Turnover

o Inventory Turnover

o Inventory Period

o Average Collection Period

o Accounts Payable to Sales (%)

o Total asset turnover (TAT) Ratio

o Fixed asset turnover (FAT) Ratio

o Sales Revenue per Employee

o Profitability Ratios, including

o Gross Profit Margin

o Operating Profit Margin

o Return on Assets

o Return on Equity

o Return on capital employed ("ROCE")

o Investor Ratios (also known

as Market Value Ratios), including

o Earnings per share ("EPS")

o Price-Earnings Ratio ("P/E Ratio")

o Price / Cash Ratio

o Dividend Yield (also known as Dividen Policy Ratios)

o Dividend Yield

o Payout Ratio

o Book Value per Share

o Market Value per Share

o Market / Book Ratio

Leverage Ratios (also called Debt Ratios)

|

Oct 2011

students

Dana A., Jelyn A. Karlo C., Rana H. Gursimran (Sim) G. presented to the CCT 224

class a description of Leverage Ratios using the theme of "Who Wants to

be a Millionaire".

|

|

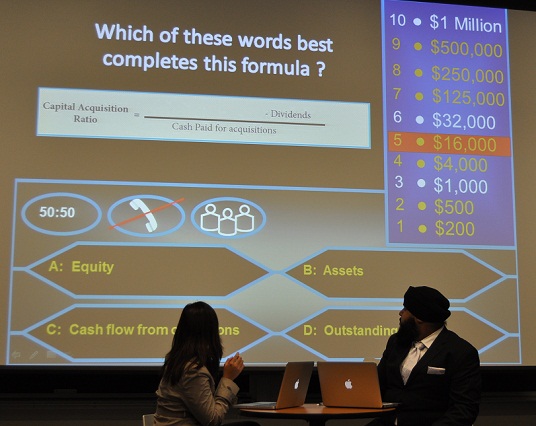

Leverage Ratios

A quick snapshot to show the elaborate PPT the student presenters created to mimic the questions in the game, and use those questions to go through the main points describing Leverage Ratios |

|

Leverage Ratios

- they even managed to get

in some audience participation by having the students shout out what one

of the answers should be to a question

Their .pdf explaining Leverage

ratios is at

|

|

Understanding

Canadian Business 7th Edition by Nickels et al

Chpt 16 |

"Leverage (debt)

ratios measure the degree to which a firm relies on borrowed funds in its

operations. A firm that takes on too much debt could experience problems

repaying lenders or meeting promises made to shareholders. The debt to

owners equity ratio measures the degree to which the company is financed

by borrowed funds that must be repaid."

Debt to Owners's equity

= Total liabilities

"Any number above 100 percent shows that a firm has more debt than equity" |

|

Oct 2011,

students

Colby H., Murtaza H. Heba I., Tashfia I. Nancy K. presented to the CCT 224 class a description of Liquidity Ratios Colby did a good job as the lead off speaker and he and Murtaza and Heba energetically explained their concepts through a board game which they had handed out to the class. The group also emphasize "something interesting learned...". Tashfia found an interesting article which discussed cash ratios. |

|

Understanding

Canadian Business 7th Edition by Nickels et al

Chpt 16 |

"Liquidity refers

to how fast an asset can be converted to cash. Liquidity ratios measure

a companys ability to turn some assets into cash to pay its short-term

debts (liabilities that must be repaid within one year).These short-term

debts are of particular importance to creditors/lenders of the firm, who

expect to be paid on time. Two key liquidity ratios are the current ratio

and the acid-test ratio."

"The current ratio is the ratio of a firms current assets to its current liabilities. The numbers used to calculate this ratio can be found on the firms balance sheet" Current Ratio =

current assests

"Usually a company with a current ratio of 2 or better is considered a safe risk for creditors/lenders granting short-term credit, since it has over two times more current assets available to pay their current liabilities." Acid Test Ratio =

cash + accounts receivable + marketable securities

"This ratio is particularly important to firms with relatively large inventory, which can take longer than other current assets to convert into cash. It helps answer such questions as: What if sales drop off and we cant sell our inventory? Can we still pay our short-term debt? Though ratios vary among industries, an acid-test ratio over 1.0 is usually considered satisfactory" |

| . | Oct 2011

students

Ermir K., Karolina K. Patrick L., Jennifer (Yan Chi) L. Eric M. (pic coming) presented to the CCT 224 class a description of Efficiency Ratios - did a good skit, unfortunately their "media" did not work out OK, but sometimes that is just bad luck - the info they had was good, but because the "technology" did not work, there was no engagement with the audience at all - each group should therefore always have a back-up-plan / contingency, such as a hand out, for these situations |

|

Oct

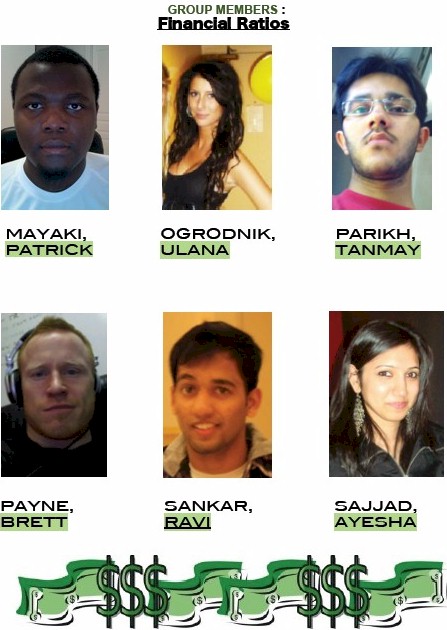

2011 students

Patrick M., Ulana O. Tanmay P., Brett P. Ayesha S., Ravi S. presented to the CCT 224 class a description of Profitability Ratios Their presentation was pretty interesting in how they made a "skit" called "Chickens Pen" which was based on Dragon's Den - good imagination - good graphics, good story line and good use of members in the group to explain all the parts of Profitability Ratios

|

click on this link to see

the PDF they compiled on Profitability Ratios

|

|

Understanding

Canadian Business 7th Edition by Nickels et al

Chpt 16 |

"Profitability

(performance) ratios measure how effectively a firm is using its various

resources to achieve profits. Company managements performance is often

measured by the firms profitability ratios. Three of the more important

ratios are earnings per share (EPS), return on sales, and return on equity"

Basic earnings per share

(EPS) = Net income after taxes

"The basic earnings per share (basic EPS) ratio helps determine the amount of profit a company earned for each share of outstanding common stock. "

|

|

Oct 2011

students

Tim S., Delaney S. Hamna T., Rocky T. Aanchal V., Harry Y., Kian Y. presented to the CCT 224 class a description of Leverage Ratios witiger.com/internationalbusiness

Liked the fact each group member wore clear name tags which allowed the prof and the audience to know who was saying what. |

|

Investor Ratios -

the video

The best thing about this

group's presentation was the video they posted on YouTube

One of the key things any professor wants to know is that if the students actually learned something useful and interesting during the course of doing some assignment, if you specifically state this in the process of writing up an assignment, it is very VERY helpful to the person evaluating your mark. |

Ratios - Alberta

Govt Source

-------------------------------------.

Investopedia.com

Financial Ratios

Tutorial

Online

by Richard Loth

http://lothinvest.com