MGTC50

Commerce Ventures

A 3rd year undergraduate course in the Division of Management, University of Toronto at Scarborough

|

|

MGTC50Commerce Ventures A 3rd year undergraduate course in the Division of Management, University of Toronto at Scarborough |

This page last updated 2001 Nov 17 Saturday

Payment

acceptance and processing

www.witiger.com/ecommerce/paymentmatrix.htm

SET and SSL

Digital

Certificates

Setting up a Shipping

Account

Forms related

to shipping and receiving

calculating shipping costs

online

the large courier

and shipping companies

.

| Section A | Section B | Section C | Section D | Section E |

| Chpt 7

Electronic Payment Systems  |

Before we begin to discuss the different

types of payment systems, let's take a perspective from the introduction

to Chapters 7 that Schneider and Perry wrote and look at one of the big

reasons why companies want to effect EPS.

The answer to that reason is the same fundamental answer to why all companies are trying variants of e-commerce - the answer is "to cut costs". A substantial amount of the costs medium and large sized companies incur is the costs associated with billing. These costs include the printing and paper costs of making the invoice/bill and envelopes, as well as the postage costs for mailing the bills. Utility companies, for example, can spend $1 to $1.50 on each customer each month sending out tens our thousands of bills. When you are able to implement an electronic payment system for these types of situations it can save a large company $X00,000's of dollars each billing cycle - in addition, you also have the environmental consideration of saving trees, literally. |

| Chapter

7

|

Schneider and Perry write in

the beginning of chapter 7 a caution that still holds true 2 years after

the book was released in Dec 1999;

"Implementation of electronic payment systems is in its infancy and still evolving. The technical, economic, cultural and legal components of electronic payment systems are not fully understood.. As a result there are a number of competing proposals for implementations of electronic payment systems"

"When customers arrive at a store's electronic checkout counter, merchants want to offer them payment options that are safe, covenient and widely accepted. The key is to figure out which choices work best for your company and for your customers" Schneider and Perry page 212- 1st Edition |

|

Payment Systems for traditionally disenfranchised people Payment

|

Patore comments ""There is a need in the market for a teen payment product that allows secure payments online," said Julie Cunningham, financial services analyst at Datamonitor. "Teens are keen to have their independence and to shop online. Both traditional players and new entrants have a part to play in this market. New entrants can attract teens through the 'cool factor', while traditional players should use their established role in society as a way to convince parents and to gain their support." Patore wrote "Datamonitor predicts that online teen payments will grow considerably in the next five years -- due in part to general growth in the number of Internet users. However, growth is likely to be very different in the United States compared to Europe. U.S. teenagers generally have much more money at their disposal than their European counterparts. The dominance of the credit card in the United States will allow products connected to parents' credit cards to flourish. In Europe, more independent solutions will emerge, with products developed by independent companies such as Smartcreds and Splash Plastic, but also from banks."

|

| Payment

Acceptance and Processing

Chpt 14

|

Creating Stores on the Web

Chpt 14, "Payment Acceptance and Processing" page 324 - 331 describes several of the

new types of payment options being used.

|

| SET and SSL

Chpt 14 |

"Netscape's Secure

Sockets Layer, SSL, provides a secure channel between web clients and web

servers ... this is an important point because unlike the standard Internet

protocols, such as TCP/IP, SSL must be selectively employed by the web

client (the person surfing)... SSL is a layered approach to providing a

secure channel"

|

| Payment

Acceptance and Processing

Chpt 14

|

Creating Stores on the Web

Chpt 14, "SET" Secure Electronic Transmission" page 336

SET - Secure Electronic Transaction,

SET vs. SSL

According to Greenstein and Feinman

(p. 297) "The initial version of SET protocol is considered to be

a stronger security mechanism than other transmission protocols, such as

SSL, because of SET's stronger authentification features". Greenstein and

Feinman point out that SSL is good at providing confidentiality during

the transmission of the data, but alone it does not authenticate either

the sender or the receiver of the message.

|

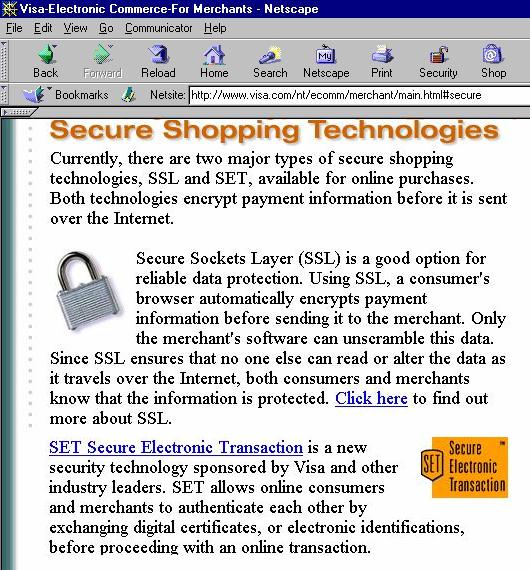

| SSL and SET according to

the credit card companies

The screen capture to the right comes from the VISA web site. Why note Visa? - because Visa has more cards worldwide than the total number of American Express, MasterCard, and Discover cards combined. |

|

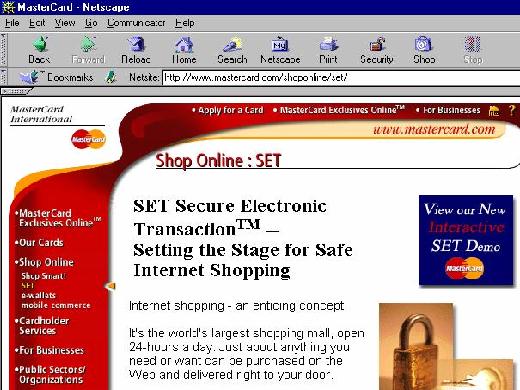

| SSL and SET according to the credit

card companies

The screen capture to the right comes from the Mastercard web site. |

|

| Digital

Certificates

Chpt 14 |

Digital Certificates

page 337

Netscape's web site has a great explanation

of digital certificates, and further explains how individual people can

obtain them for security in communication.

"A digital certificate is a software tool that you can install in your browser. Once installed, your digital certificate identifies you to web sites equipped to automatically check it. A digital certificate

|

| Shipping

Chpt 17 |

Chpt 17, page 377 Creating Stores on the Web "Online means mail order, and mail order

means shipping. And, being an online store, you will have customers all

over the world -- some in very remote places. A significant number

of them will be used to the immediate gratification of the Web, and

that means being able to get them your goods as soon as possible. The

speed with which you can deliver their orders can be critical to

your business' success. Shipping is one of the few things that links

you physically with your customers. While pricing, promotion, communication,

and order processing can be done virtually, the shipped package is

what your customers will hold in their hands.

The same level of speed, quality, and attention to detail you put into the Web-based portion of your store also needs to be applied to the shipping side. You should understand that no single shipping option can cover you completely and provide maximum efficiency. The challenge is to stitch together the various services, software, Web sites, and your own store into a unified model that allows customers the best coverage, speed, and pricing options. Then you have to display this "shipping stew" on your site in a manner that is easy for your customers to understand. A Web site with too many options or too few instructions is confusing to customers. When someone looks lost in a real store, the owner will notice and be able to physically respond. On the Web you won't. Customers will turn away without your even noticing as they find that you don't offer a particular option for delivery. All you will notice is lower sales. All of these are reasons why something as mundane and physical as how you organize your shipping plan is incredibly important to your store. So get to know your solutions inside and out, use the Web as much as you can, and make sure your plan is clearly displayed to users. If you maintain that and utilize the software the shipping companies offer, your customers will get nicely packaged, on-time products, and you'll get repeat business. Many of the posts on newsgroups and much of the positive e-mail Tronix has received from its customers concerns its attention to the details of shipping." Some of the text words above come from

|

| Shipping

Chpt 17 |

Chpt 17, Setting up a Shipping Account

|

| Shipping

Chpt 17 |

Chpt 17, Setting up a Shipping Account Linking Shipping with Your Web Site

|

| Shipping

Problems calculating the cost Shipping Problems

|

Morphy writes "Jupiter Media Metrix statistics show that 63 percent of online shoppers back out of a purchase when they see how much they have to pay for shipping and handling. In fact, the high cost of shipping -- and the almost surreptitious, last-minute manner in which it is sprung on the shopper -- is one of the major customer complaints about online retailers." Morphy explains "... the problem is really

that consumers, perhaps subconsciously, resent paying

any

|

| Shipping

What do you

|

What do you do when you are outside

the territory they ship to

From their web site, Borderfree.com says

www.borderfree.com/bf2/jsp/com_au_our_company.jsp

who are customers of bordefree.com, companies like RitzCamera.com and BoatersWorld.com in class we will go online to RitzCamera.com and show the process |

| Shipping

the large courier and shipping companies UPS and FEDEX account for more than 80 % of online shipment deliveries |

UPS - www.ups.com FedEx - www.fedex.com DHL - www.dhl.com Canada Post www.canadapost.ca |

|

The UPS page which covers FAQs and other required info |

|

The FEDEX FAQ page

-they specify "Canadian" English !! |

|

The FEDEX page describing the products they offer to people shipping to Canada |

| Shipping

Chpt 17 Returns

Shipping

Returns

|

Chpt 17, page 397 Creating Stores on the Web Refunds

Creating Stores on the Web Chpt 17, page 398 "If you do happen to make a mistake on

a customer's shipping address, forget to check off the appropriate method

of shipping, or send them an incorrect item or quantity, show deep concern,

apologize profusely, and offer the customer free shipping on the next order..."

#4 Plan for the flood.

#5 Deliver, deliver, deliver.

#6 Make return policies easy and efficient.

#10 Create a service recovery system.

|

| Shipping

The effects of

|

Morphy writes "Forrester Research was not overly enthusiastic about holiday shopping prospects for online retailers -- even before September 11th. Now, the consulting company is warning of another problem that could affect consumer confidence unless retailers take proactive measures: shipping. " Security Delays: Heightened security at ports, fortunately, is only delaying shipments by hours, not days -- so far. If U.S. Customs starts turning spot checks of containers into full searches, however, holiday orders could be delayed until it is too late, Forrester warned. Aircraft used in shipping: Another

possible cause of delays is the Civil Reserve Air Fleet

"Forrester also predicted new shipping-related services will develop in the long run that will change holiday shopping patterns for retailers and consumers. Buying cycles will change, the consulting firm forecast, as shoppers buy and ship for the holidays throughout the year to get their gifts on time. " |

||||

| Shipping

The effects of

|

"While there are no easy answers, the Ontario Trucking Association is now calling upon motor carriers, drivers and shippers to work together to ease the pressure at congested border crossings and keep essential deliveries moving as seamlessly as possible. "The backlog of trucks at the major Ontario-U.S. border points is testing the limits of the North American distribution network, and no one is expecting things to change in the foreseeable future," OTA president David Bradley said. For that reason, the OTA is stepping in to help Canadian federal and provincial authorities ensure that essential shipments receive priority attention." |

| Shipping |