m-payment systems 2006

| M-COMMERCE

m-payment systems 2006 |

|

|

This web page has audio clips - just click on the icon (like the one to the left) and you can hear Prof. Richardson's voice adding additional information to topics on the page. |  |

turn on your speakers to hear audio clips |

| . | This page

used in the following courses taught by Prof. Richardson

.

|

| INTRODUCTION

|

, | Since 1999 I

have been advocating to my e-commerce students that Canada could become

a world leader in the launching of a system whereby you could use your

cellphone as a debit device and pay for things with your phone much like

you could use your interac card. I championed this development for several

reasons.

1. Canadians invented the phone.... Alexander Graham Bell, duh... 2. Canadians invented the cell phone ... not many know this 3. we have an oligopoly among our banks which is bad in some ways, but good if you want to launch a national payment system cause you only need 5 playaz to agree, RBC, CIBC, BMO, TD & Scotiabank 4. young Canadians use the internet at a very high percentage, thanks to gov't funding for the internet in public school and high schools 5. Canadian businesses adopted, and used debit cards at a much higher rate, and earlier than U.S. businesses - we found it "no problem" to swipe 6. our telecomm companies have lots of money and are very competitive, always striving for new technologies to exploit 7. some people think Canadians are conservative, but when it comes to money stuff, we try all sorts of new and weird things - we use Canadian Tire money, we turn our dollar bill into a coin, then we have a toonie - we pay our bills over the internet, we use swipe cards for transit, we have contactless payment systems at gas stations - we try a lot of new 'tings. So for all these reasons I told my students in 2000, 2001, 2002, 2003, 2004 and 2005 that they should read the newspapers on a regular basis and watch for companies that might be involved because those would be good companies to work for, or at least buy stock from. |

| INTRODUCTION

|

, | Now in 2006

it seems to be coming together in several ways in Canada - however.......

we need to keep in mind that in Asia and Europe and Africa, there have

been developments there that will effect us in terms of the

My hope from the Rogers, Bell and TELUS consortium is not simply a copy of DoCoMos phone that carries an eCash function but rather something more spohisticated - that is to say your phone will allow you to debit money directly from your account at Royal Bank or CIBC -whatever, so there is no intermediate step of having to load the phone with money - the phone simply acts as an intermediary device between the vendor and your bank, just like how we use interac cards presently. |

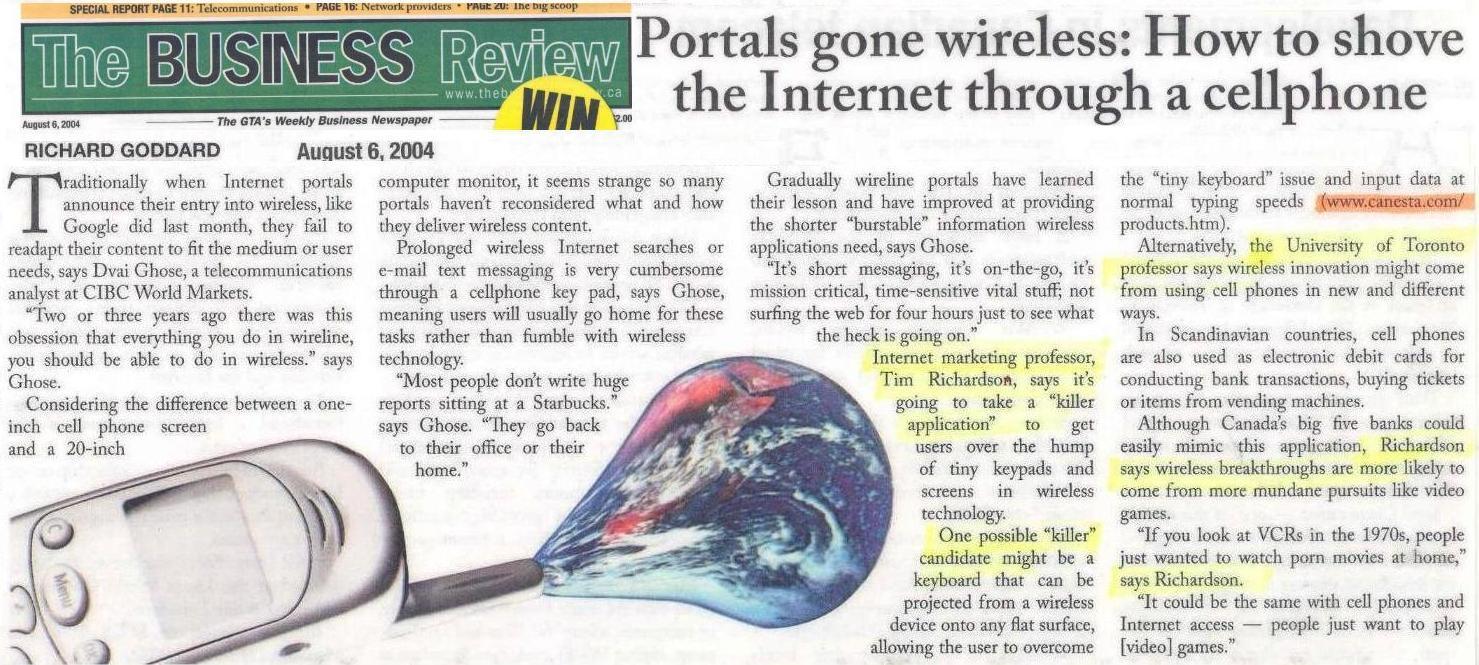

| 2004 | , | In the summer of 2004, Prof.

Richardson was interviewed by the Business Review for some articles related

to m-commerce. Richardson suggested that before m-commerce payment systems

"take-off", there has to be a strong reason why people would want to use

their cell phone as a payment device through the Internet - in a sense,

a "killer application".

|

| Read the article to the right which features an interview given by Prof. Richardson in August 2004 re: the challenges in developing payment systems for mobile commerce (m-commerce). |  |

| The

Situation in Canada 2005 |

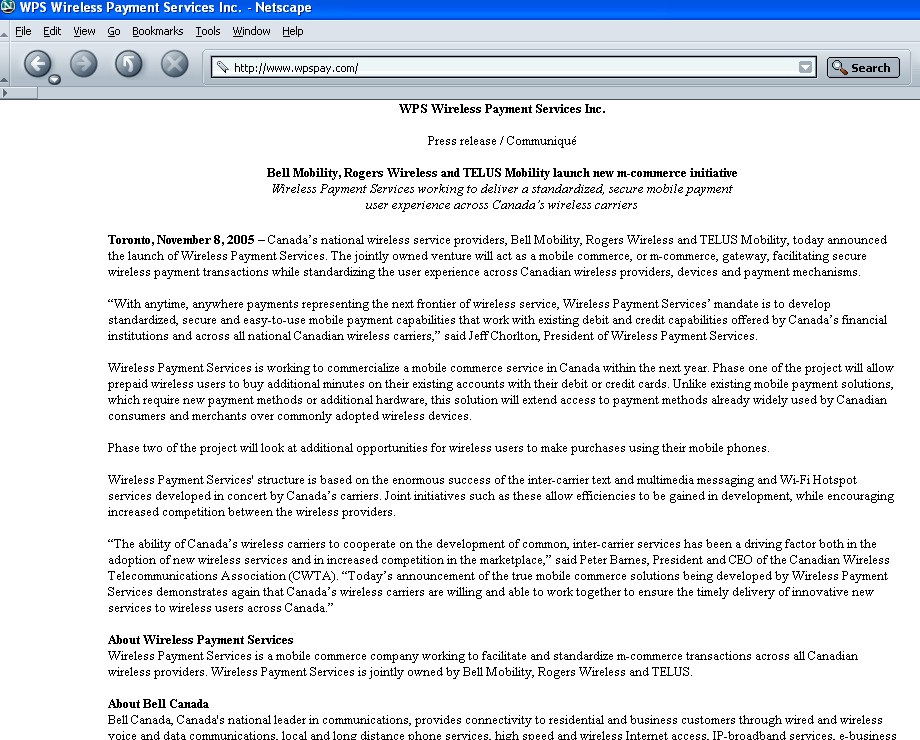

b | So, moving forward

from 2004 to November 2005,

"Canada's national wireless service providers, Bell Mobility, Rogers Wireless and TELUS Mobility, announced the launch of Wireless Payment Services. The jointly owned venture will act as a mobile commerce, or m-commerce, gateway, facilitating secure wireless payment transactions while standardizing the user experience across Canadian wireless providers, devices and payment mechanisms". http://www.wpspay.com/

was launched in Nov 2005, BUT..... 7 months later, it is still a single

page website with the old press release

|

| Industry

Consortium Approach |

management consulting

firm Booz Allen Hamilton suggests an Industry Consortium Approach explaining

that "The single most important step in building a successful m-payment

system is to set the incentives for all stakeholders. Without this, there

will be no progress."

Booz Allen Hamilton outlines the role that 5 key players need to take Banks and credit card companies ..."must leverage existing value chains, rather than build new competitive solutions. They must also evaluate ways to let mobile telecoms participate in collaborative value generation." Mobile operators "must consider new mobile payment systems in the context of new ways to open up revenue streams, especially from monthly m-payment subscription charges or per transaction fees. Operators must also take full advantage of the positive side effect of embedding the mobile phone even deeper into the life of the subscribers a significant motivator in the Japanese model." Handset suppliers [cellphone makers] "must embrace new approaches and start to consider active integration of mobile payment capabilities into product road maps and line-ups. Mobile payment capabilities are seen by some as the next big thing to drive handset replacement, making standardization and compatibility across operators and platforms critical to preserve user attractiveness and scale benefits." Merchants "must use their vast experience with cashless payments to drive further cost decreases that accrue from giving up cash, and to offset POS technology upgrade costs." Customers: "it needs to be demonstrated to mobile phone users that mobile payment is much more attractive than other more familiar payment schemes. The bundle of convenience aspects (safe, secure, available, fast, transparent, etc.) needs to be packaged and sold to target groups individually." by Roman Friedrich, Johannes Bussmann, Olaf Acker, and Niklas Dieterich |

| Update

June 2006 |

So June 16th,

2006 I get called by a young journalist, Brett Popplewell who has just

graduated from Carleton and he calls me from his new office at Canadian

Press to inquire about background for a story about credit cards with chips

and other developments in the credit card payment arena. I tell him some

things but suggest that developments in credit cards will be eclipsed by

the technical advances in cell phones and suggested to Brett that if he

has room in the article that he should finish with an angle about how Canada

is well positioned with the big cell phone companies and an oligopoly among

the banks.

Anyhow, CP puts a story out on the wire and it is picked up by several newspapers across Canada, |

|

WIRELESS BANKING Africa 2005

|

Nicole Itano, The Christian Science Monitor

"A 2003 survey estimated that only half of South African adults had a bank account, but a third of those without an account owned a mobile phone. Cell phones have spread quicker than bank accounts across the rest of Africa. FinMark, a British-backed non-governmental organization that looks at ways financial markets can help the poor, estimates at least half of all bank accounts in South Africa will be administered via cell phones within five years. MTN (MTNJ.J), Africas biggest mobile operator by sales, hopes the new banking service will serve as a retention tool for existing high-spending cell phone customers. |

| WIRELESS

BANKING Africa 2005

|

Finmark expects

the new technology to attract a rush of demand from low earners, who critics

say have been neglected by big banks focused on more lucrative business."

The story appears to be written by By Rebecca Harrison but it has been carried on so many online sites it is difficult to know the original host. It appeared on the Pakistan newspaper Daily Times Nov 6th, 2005. Was also carried on yahoonews Nov 1st. Permission to quote from Yahoo!, use the Yahoo! logo, and use screen captures, was given in an email by Debbie Macleod, Yahoo! Marketing Manager Jan 21st, 2005. Copy of the email is kept in the permissions binder "Cell phones are already used for music downloads, text messaging, and video games. But here in South Africa, they are beginning to perform another function: personal piggy bank. With the new technology, a grandmother in rural area can receive money from her son, working hundreds of miles away, with the beep of her cell phone. A teenager can buy groceries with a few punches of keys. Not a coin need change hands. It's a high-tech solution

designed to help poor people here who never have had access to banks, cash

machines, or credit cards. And it's another example of using digital technology

to fast forward development in remote areas."

|

Japan

Korea

|

in late 2002

Japanese wireless carrier NTT DoCoMo launched the world's first service

that lets people withdraw and deposit money at cashpoints in convenience

stores and supermarkets using mobile phones instead of cash cards.

/www.cellular.co.za/news_2002/082202-doCoMo-cashpoint-access.htm "While the idea of using

a mobile phone as a credit card makes the collective North American Consumer

a bit nervous, Japan has already embraced and implemented the practice.

NTT DoCoMo announced last month [Dec 2005] that consumers may swipe their

cell phones at any RF enabled reader."

"M-payments are catching

fire in Japan and Korea, but have so far failed to spark much interest

in Europe and the U.S. The efforts in those two regions have faltered mainly

for two reasons: The technology wasnt in place, and the stakeholders

banks, credit card issuers, handset makers, and telecommunications companies

have worked at cross purposes. But all thats changing. Recent advances

in handset, chip, and mobile network technologies and upgrades to the point-of-sale

infrastructure along with better teamwork among the players have dramatically

improved the environment for mobile payment solutions across the globe."

|

| Japan

|

Lessons from

Asia

"To understand why m-payments face an uphill battle in Europe and the U.S., its instructive to understand why theyre taking off in Japan and Korea. The chief driver of mobile innovation in Japan is NTT DoCoMo, far and away the countrys leading wireless provider. So dominant is its position that DoCoMo can impose a new system from the top down, as it did in 1999 with i-mode, its breakthrough digital data service, which now claims 45 million subscribers. Although i-mode did not initially provide for mobile payments, it successfully laid the groundwork with customers for that functionality. The latest step in the evolution of the cell phone is DoCoMos venture with Sony. The wireless company is now implanting Sonys FeliCa contactless chips, which were initially used in public transit smartcards, into its cell phones, giving customers the ability to pay for train fare, theater tickets, and a growing array of other products by passing their phones over a sensor. The results are impressive: Five months into the program, at the end of 2004, DoCoMo had sold more than 1 million FeliCa-equipped phones and expects to hit 10 million by the end of 2005, exceeding the rate of adoption of the wildly popular i-mode. The important point here is that NTT DoCoMos complete dominance of its market allows it to impose its new cashless, contactless payment scheme from the top down with relative ease. Customers, whove had six years to get used to using their phones as lifestyle tools rather than just as communications devices, have demonstrated that theyre eager to take advantage the m-payment function. Merchants want to tap into a large and growing market (DoCoMo tempted those who werent initially ready to pay for the new point-of-service technology with subsidies). And DoCoMo didnt need the buy-in of banks and credit card companies at the outset to make the whole thing fly (although it does plan to work with both to expand its business beyond the prepaid model)." by Roman Friedrich, Johannes Bussmann, Olaf Acker, and Niklas Dieterich |

| Japan

2004

|

AP

journalist Yuri Kageyama wrote an article July 22, 2004 in which he

described using one of the new DoCoMo phones.

To pay you simply wave your cell phone within a few inches of a special display found in stores, restaurants and vending machines around Japan. A fairy-like tinkling sound means your purchase is being deducted from the embedded chip using radio-frequency ID technology. Unlike infrared or other mobile payment schemes that require clicks on the handset, you don't even need to open your clamshell-shaped phone, the style of choice here." Kageyama says "It's also an idea that makes sense, given that almost every Japanese has a cell phone and relies on it for so much information that being stranded in the street without one almost causes panic. There are 81.5 million cell phones in this nation of 127 million people. For the wallet phone tech to really take off, stores, theaters and restaurants that accept electronic payments need to become more widespread. They total around 9,000 in Japan so far, but the number is quickly growing. To buy a diet Pepsi from a vending machine, I pushed a button on the machine that indicates electronic payment and pushed another button to pick the soda. When a display the size of a small greeting card lit up with the price, I put my phone next to the display. The soda pop rolled out, and the display blinked with the amount of money left in the phone. "b |

Korea

|

"The situation

in Korea is slightly different. All three of the countrys biggest

mobile operators, SK Telecom, KTF, and LG Telecom, are now offering cell

phones that can be used as credit cards and FeliCa-style prepaid smartcards.

While telecommunications companies are driving the new systems, theyre

working arm-in-arm with credit card companies, which are taking

care of the financing and operations, taking less than half their usual

2.5 percent cut. One percent goes to subsidize the cost of the phones for

customers, and 0.3 percent goes to the telecoms, which own the m-payment

technology, leaving just 1.2 percent for the credit card companies. But,

for now at least, that highly cooperative arrangement works well for everyone

as the stakeholders join together to build their customer bases and increase

revenues."

by Roman Friedrich, Johannes Bussmann, Olaf Acker, and Niklas Dieterich |

| Russia

|

Russia's largest

bank, Sberbank (Savings Bank of the Russian Federation) www.sbrf.ru

has developed [Jan. 2006] a venture with Visa International, and MegaFon

Moscow,

"Through this new product

the holders of Sberbank-issued Visas who are using the Mobile Bank service

get new opportunities to pay for products and services from their mobiles

at any location where mobile communication is available.

|

On this page there are several quotes from ecommercetimes.com. Permission was given by Richard Kern, Associate Publisher of the E-Commerce Times, in an email to Prof. Richardson 2004 Dec 10th, a hard copy of the email is kep on file in Richardson's permissions binder.

On this page there are several

quotes from management consulting firm Booz Allen Hamilton, Europe

from http://www.strategy-business.com/resilience/rr00023

by Roman Friedrich, Johannes

Bussmann, Olaf Acker, and Niklas Dieterich

permission to quote given

by Dr. Friedrich in emails June 22, 2006, copies kept in the Permissions

Binder

|

|

CONTACT I MAIN PAGE I NEWS GALLERY I E-BIZ SHORTCUTS I INT'L BIZ SHORTCUTS I MKTG&BUSINESS SHORTCUTS I TEACHING SCHEDULE |

| . | |

| MISTAKES I TEXTS USED I IMAGES I RANK I DISCLAIMER I STUDENT CONTRIBUTORS I FORMER STUDENTS I | |

| . |